We’ve been warned about the new 1099-K reporting thresholds for over a year now. However, there is one payment app that is not included in these new policy changes: Zelle. In this article, we’ll give an overview of Zelle, including its features, why it is not required to abide by the new thresholds, and if it’s the right payment app for you.

What are the new 1099-K reporting thresholds?

As part of the American Rescue Plan of 2021, the IRS announced some new reporting thresholds for Form 1099-K. Prior to 2023, Form 1099-K, otherwise known as the Payment Card and Third-Party Network Transactions form, is automatically sent out by financial institutions if you earned an aggregate amount of $20,000 in over 200 transactions for goods and services. They are using 2023 as yet another transition year. In tax year 2024, the threshold for IRS Form 1099-K will be $5,000. This increase will serve as a phase-in for the $600 threshold in the future.

What is Zelle?

Zelle is a digital payment network controlled by a group of banks. These include Bank of America, Capital One, JPMorgan Chase, Wells Fargo, U.S. Bank, and a few others. It allows users to send funds directly to other users, even if they do not have the same bank and even if their bank does not offer Zelle. All you need is the recipient’s email address or phone number to safely send money.

Why is Zelle exempt from the new 1099-K reporting thresholds?

So, why is Zelle exempt from this? The answer to this lies in the method they use to transfer funds. With apps like Venmo, PayPal or Etsy, you receive funds in exchange for goods and services. Then those funds are held in the app until you transfer the funds to your bank account. Zelle, on the other hand, does not hold funds. Instead, they do direct bank transfers between users and these transactions are not subject to the IRS’s 1099-K reporting requirements.

Can I switch to Zelle to avoid receiving a 1099-K?

Remember, just because you don’t receive a 1099-K for income earned, does not mean you are exempt from reporting your income to the IRS or paying taxes on it. The last thing you want is an IRS audit or worse: the IRS pursuing criminal charges for deliberate concealment of taxable income.

Tax Help for Those Who Use Zelle and Other Third-Party Payment Apps

Although we haven’t technically experienced the new change, it is already in effect. If you receive payments through third-party payment apps other than Zelle, you should expect to receive a 1099-K if you earned within the reporting threshold. If you currently collect payments for your small business through Zelle, you will not receive a 1099-K. But beware that this does not mean you are off the hook when it comes to paying taxes. It means you have the additional responsibility of calculating the income earned through Zelle and reporting this income to the IRS during tax time. Optima Tax Relief is the nation’s leading tax resolution firm.

If you’ve never heard of the State and Local Tax (SALT) deduction, you’re not alone. But if you have, you may know that it is a topic that often raises eyebrows and sparks debates. For many taxpayers, the SALT deduction plays a significant role in their financial planning and overall tax liability. This is especially true for those who live in a high-tax state. In this article, we’ll delve into the intricacies of the SALT deduction, exploring its mechanics, controversies, and potential implications for taxpayers.

What is the SALT deduction?

The State and Local Tax (SALT) deduction allows taxpayers to deduct state and local taxes from their federal taxable income. These deductible taxes typically include state and local income taxes, property taxes, and sales taxes. One key thing to note, however, is you may only deduct either state and local sales taxes or state and local income taxes, but not both. The deduction aims to provide relief to taxpayers by preventing double taxation. In other words, it helps prevent paying taxes at both the state and federal levels on the same income. Taxpayers can deduct up to $10,000 in 2023, or $5,000 if they are married but filing separately. Remember, you may only take the SALT deduction if you itemize your deductions.

What does the SALT deduction cover?

The SALT deduction typically covers the following types of taxes:

Income taxes: Whether you are a W-2 employee or self-employed, you’ll be able to find out how much state or local income tax you paid over the tax year.

Property taxes: This tax is a little more complicated and does not come with much guidance from the IRS who advises that some types of payments do not qualify.

Personal property taxes: Typically, you can deduct taxes paid on personal property like a vehicle.

Sales taxes: Deducting sales tax usually requires keeping excellent records. Some taxpayers prefer to deduct state and local income taxes instead because it’s usually calculated for them at the end of the year. However, this is particularly beneficial for individuals residing in states without a state income tax. This is because they can deduct their sales taxes instead.

Key Points

While these are the primary taxes covered by the SALT deduction, there are limitations.

The Tax Cuts and Jobs Act (TCJA) of 2017 introduced a cap on the SALT deduction. It limited the total deductible amount to $10,000 for both single and married taxpayers filing jointly. This cap significantly impacted taxpayers in high-tax states who were accustomed to deducting larger amounts.

Taxpayers must itemize their deductions on their tax returns to claim the SALT deduction. This means that individuals who choose to take the standard deduction won’t be able to benefit from the SALT deduction.

Taxpayers can choose either the state and local sales tax deduction or the state and local income tax deduction, but not both. The choice is typically based on which option provides a higher deduction amount.

The SALT deduction is subject to potential changes in tax law and policy.

Need Tax Help? Call Optima.

While the SALT deduction provides relief to many taxpayers, its limitations and potential changes have led to ongoing debates about its fairness, distributional impact, and its effect on federal revenue. Taxpayers should stay informed about changes to tax laws and consult with tax professionals to make the most informed decisions regarding their deductions and overall tax planning strategies. If ever unsure about which deductions you are allowed to take, contact an expert tax professional. Optima Tax Relief is the nation’s leading tax resolution firm with over a decade of experience helping taxpayers with tough tax situations.

Today, Optima Tax Relief’s Lead Tax Attorney, Phil Hwang, discusses private collection agencies, otherwise known as PCAs.

Unbeknownst to some taxpayers, the IRS doesn’t always collect taxes on their own. Sometimes they hire private collection agencies (PCAs). The IRS contracts these agencies to collect overdue tax debt from individuals and businesses.

That said, if a collection agency contacts you and they are not the IRS, you should still take the warning seriously. Keep in mind that the IRS currently only utilizes the services of three PCAs:

CBE Group Inc.

Coast Professional, Inc.

Conserve

If another company is trying to collect on the IRS’s behalf, you should report them to the IRS immediately. The IRS will send you Notice CP40 to let you know that your overdue tax account has been assigned to a PCA.

Taxpayers should keep in mind that once the IRS assigns their account to a PCA, they will no longer be able to claim hardship or submit an offer in compromise. However, getting your case back to the IRS is possible and should be considered if you want the best possible resolution.

Join us next Friday as Phil will answer your questions about tax deductions, including how to maximize them!

If Your Tax Account Has Been Assigned to a PCA, Contact Us Today for a Free Consultation

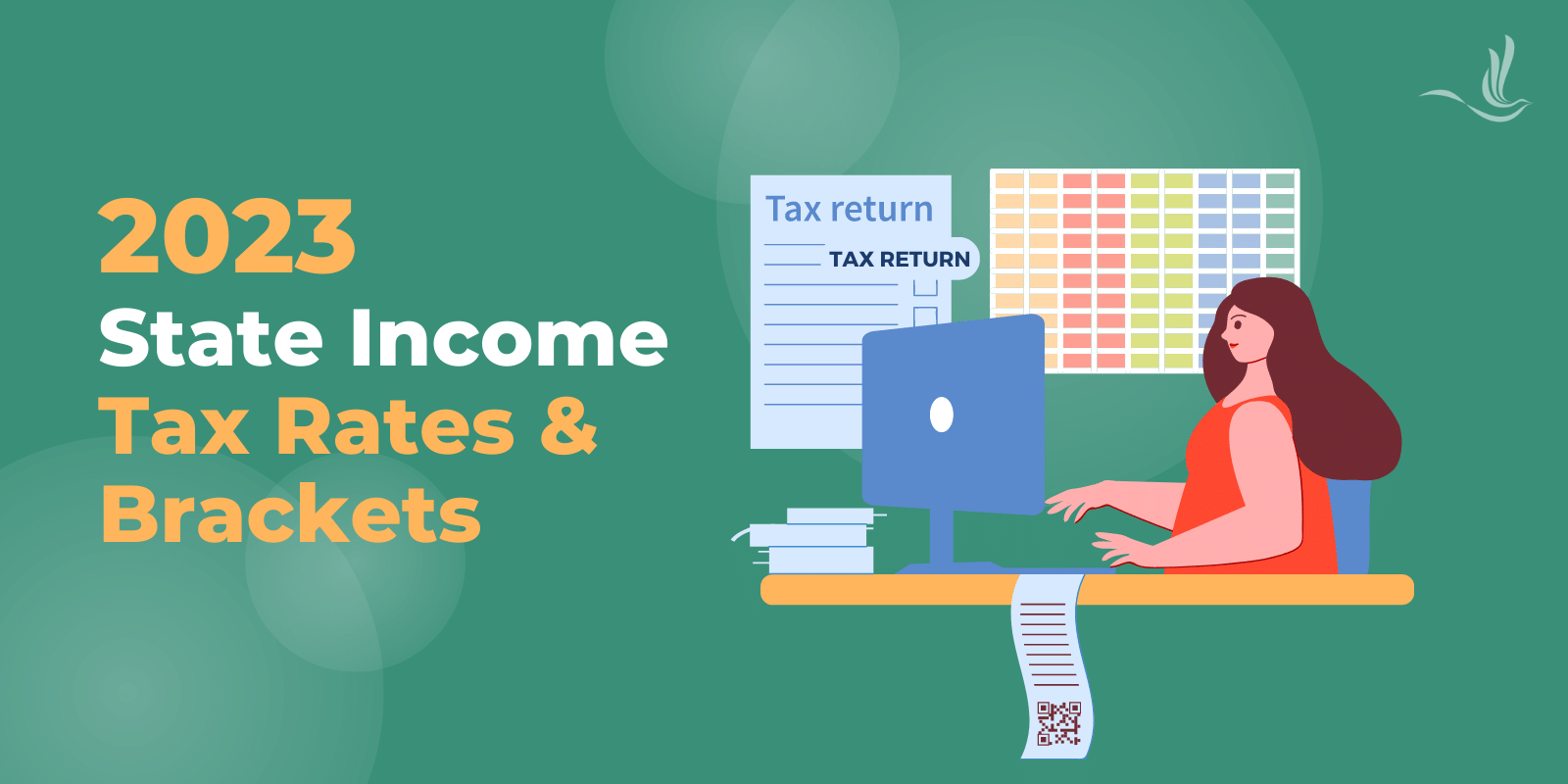

We often discuss federal taxes here, from tax filings to deductions and credits. However, it’s important to note that federal taxes are typically only one half of a taxpayer’s responsibility. In addition to filing and paying federal taxes each year, taxpayers must also stay on top of their state tax responsibilities if they have any. Here we will discuss the different types of state tax systems, as well as the 2023 state income tax rates and brackets.

State Tax Systems

Not every state taxes their residents the same. In fact, some states don’t tax at all. These states include Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming. New Hampshire does not tax regular income, but it does have a 5% tax on dividend and interest income. All other states either use a flat tax system or a progressive tax structure.

Flat Tax System

The flat tax system is the simpler of the two and involves one tax rate for most types of income. The factor that could change state to state is which income is considered taxable. Some states alternatively tax according to AGI instead of taxable income. States that have a flat tax rate in 2023 are:

Arizona – 2.5% of taxable income

Colorado – 4.4% of taxable income

Idaho – 5.8% of taxable income

Illinois – 4.95% of taxable income

Indiana – 3.15% of taxable income

Kentucky – 4.5% of taxable income

Michigan – 4.05% of taxable income

New Hampshire – 4% on dividends and interest income only

The remaining states use a progressive tax system, in which higher incomes are taxed at higher rates. In 2023, states that use a progressive tax system are:

State

Tax Rates

Number of Brackets

Alabama

2%-5%

3

Arkansas

2%-4.9%

3

California

1%-12.3%

9

Connecticut

3%-6.99%

7

Delaware

0%-6.6%

7

District of Columbia

4%-10.75%

7

Georgia

1%-5.75%

6

Hawaii

1.4%-11%

12

Iowa

4.4%-6%

4

Kansas

3.1%-5.7%

3

Louisiana

1.85%-4.25%

3

Maine

5.8%-7.15%

3

Maryland

2%-5.75%

8

Massachusetts

5%-9%

2

Minnesota

5.35%-9.85%

4

Mississippi

0%-5%

2

Missouri

1.5%-4.95%

8

Montana

1%-6.75%

7

Nebraska

2.46%-6.64%

4

New Jersey

1.4%-10.75%

7

New Mexico

1.7%-5.9%

5

New York

4%-10.9%

9

North Dakota

1.1%-2.9%

5

Ohio

0%-3.99%

5

Oklahoma

0.25%-4.75%

6

Oregon

4.75%-9.9%

4

Rhode Island

3.75%-5.99%

3

South Carolina

0%-6.4%

3

Vermont

3.35%-8.75%

4

Virginia

2%-5.75%

4

West Virginia

3%-6.5%

5

Wisconsin

3.54%-7.65%

4

Conclusion

Taxpayers should ensure that they stay on top of their state tax obligations as well as their federal. We often hear horror stories about what happens if the IRS begins to take collection action against you, but state tax agencies can be just as intimidating. Like the IRS, your state’s department of revenue can levy and penalize you. In addition, they can revoke or refuse to renew any state-issued licenses, including driver’s licenses and professional licenses you may need to operate a business. If you’re behind on your state taxes, Optima Tax Relief can help.

As the golden years approach, seniors and retirees face a new set of financial challenges, with tax planning becoming increasingly important. Understanding the tax implications of retirement income sources, investments, and deductions can significantly impact a retiree’s financial well-being. In this blog post, we’ll explore some valuable tax tips specifically designed for seniors and retirees, helping them navigate the complex tax landscape and make the most of their hard-earned money.

Know Your Retirement Income Sources

Before diving into tax planning, it’s crucial for seniors and retirees to identify their sources of income during retirement. Common income streams may include Social Security benefits, pensions, 401(k) or IRA distributions, annuities, investment income, and part-time employment. Knowing where your money comes from will enable you to plan effectively for tax obligations.

Understand How Tax Filing Changes

Did you know that after turning 65, you and/or your spouse can get a higher standard deduction. The 2023 standard deduction for those 65 and older is $1,850 more if you file single or head of household and an additional $1,500 per qualifying individual if you are married or a surviving spouse. These increases also apply to blind taxpayers. Taxpayers who are both 65 or older and blind will receive double the extra amount. In addition, being 65 years or older allows a taxpayer to use Form 1040-SR. While Form 1040-SR uses the same set of instructions and schedules as Form 1040, it is printed with larger text, potentially making it more accessible for seniors and retirees. It also includes the additional amount in the standard deduction.

Understand Social Security Taxation

For many retirees, Social Security benefits serve as a vital income source. However, depending on your total income, a portion of your Social Security benefits may be taxable. According to the IRS, only up to 85% of your Social Security benefits may be taxed. To determine your taxable Social Security benefits, calculate your combined income, which includes your adjusted gross income (AGI), non-taxable interest, and half of your Social Security benefits. Refer to the IRS guidelines or consult a tax professional for assistance in understanding your specific tax obligations related to Social Security benefits.

Embrace Tax-Advantaged Retirement Accounts

For retirees who have yet to withdraw funds from their retirement accounts, such as Traditional IRAs or 401(k)s, they can benefit from tax-deferred growth. However, after turning 72 (due to recent legislation changes), retirees must start taking required minimum distributions (RMDs) from these accounts, which are subject to income tax. Additionally, consider Roth IRA conversions strategically to minimize future tax burdens and leave a tax-free legacy for heirs.

Leverage Health Savings Accounts (HSAs)

If you have a high-deductible health insurance plan, consider contributing to a Health Savings Account (HSA). HSAs offer a triple tax advantage: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. Seniors can utilize their HSA funds to cover eligible medical costs in retirement, providing substantial tax savings.

Take Advantage of Catch-Up Contributions

For seniors who aim to boost their retirement savings before they retire, catch-up contributions are a valuable tool. Individuals aged 50 and above can contribute additional funds to their IRAs and workplace retirement accounts, allowing them to save more while reducing their taxable income. In 2023, you may contribute an additional $7,500 to a 401(k), 403(b), most 457 plans, and a government Thrift Savings Plan. Those who participate in SIMPLE plans can contribute $3,500 in catch-up contributions.

Deduct Medical Expenses

Medical expenses can quickly add up for seniors, making them potential tax deductions. If your total medical expenses exceed a certain percentage of your adjusted gross income, you may qualify for a deduction. Keep records of all qualifying medical costs, including doctor visits, prescription medications, long-term care expenses, and insurance premiums, to take advantage of these deductions.

Tax Help for Seniors and Retirees

As seniors and retirees embark on their new journey of financial freedom, understanding the intricacies of tax planning becomes paramount. By following these tax tips and consulting with a qualified tax professional, retirees can make informed decisions, optimize their savings, and minimize tax-related stress. Optima Tax Relief is the nation’s leading tax resolution firm.