There are instances where income will not be taxed, whether or not you report it during tax season. Understanding which earnings are taxable versus non-taxable could save you a lot of time and trouble when you file your tax returns.

In order for income to be considered non-taxable, it must be legally exempt.

Taxable vs Non-taxable Income

Some examples of taxable income would be employee wages, or constructively received income. Constructively received income is income that is available to you before the end of the tax year. This could be in the form of cash or deposit.

If an agent receives income on your behalf, this is called assignment of income. Assignment of income is still taxable, even if a third party is accepting your earnings.

Prepaid income is another taxable compensation that may include payment for future services.

Are royalties non-taxable income?

Copyrights, patents, and other properties such as oil and gas are examples of royalties. These items are taxable as income.

Are business and investment earnings non-taxable?

Business earnings such as rental properties and other investments are very much taxable. Business owners are required to pay taxes quarterly to cover Social Security and Medicare tax.

While non-profit agencies are tax exempt, you still have obligations to file a return.

What to do if you have a tax liability?

Taxable and non-taxable income can be a confusing topic. It’s best to ask a professional for assistance if you’re unsure about how or when to report income. Should you find yourself in the midst of a tax liability that is unaffordable, give Optima a call at (800) 536-0734 for a free consultation.

If you’re facing financial hard times, your retirement funds begin to look like a good source of much-needed cash. In cases of dire emergency, you may indeed be able to make withdrawals from those funds before you reach retirement age. However, the potential short-term and long-term consequences can be severe. Nonetheless, if you must make an early withdrawal from an Individual Retirement Account (IRA) or 401(k), there are certain circumstances under which you can minimize the bite by Uncle Sam.

The COVID-19 pandemic and the 2020 CARES Act have made it easier for taxpayers to withdraw funds from their retirement accounts. Learn more about taking a CARES Act retirement withdrawal HERE.

3 Types of Retirement Funds

There are three primary types of tax-optimized retirement funds in the United States:

Traditional IRAs

Roth IRAs

401(k)s

Traditional IRAs

Traditional IRAs are drawn from pre-tax earnings. When you deposit funds in a traditional IRA, the taxes on those funds and your earnings are deferred until after you retire, presumably when your income is lower and you qualify for a lower tax bracket.

Roth IRAs

By contrast, Roth IRAs are drawn from post-tax earnings. Because you pay taxes on Roth IRA deposits upfront, you do not have to pay taxes on either the principal or the earnings, provided that your Roth IRA has been open for five years or longer and you are at least 59 ½ years old when you begin making withdrawals.

401(K)

401(k) funds are sponsored by your employer. You can invest either pre-tax earnings or post-tax earnings, with tax implications similar to those for a traditional or a Roth IRA. Many employers match their employees’ contributions dollar for dollar. The catch is that you can’t access your employer’s contributions to your 401 (k) until you are fully vested in the company, which translates to being employed for a certain length of time which varies but five years is common.

For what reasons can you withdraw from an IRA without penalty?

If you are younger than age 59½, taking withdrawals from either a traditional or Roth IRA or from a 401(k) will usually trigger a 10 percent tax penalty in addition to paying any income taxes that are due. However, there are exceptions that vary depending on whether you are withdrawing from a traditional or a Roth IRA or from a 401 (k). You can avoid tax penalties from withdrawing from a traditional IRA even if you are younger than age 59 ½ for the following reasons

Purchasing a first home.

Educational expenses for yourself or a family member.

Death or disability of a family member.

Covering unreimbursed medical expenses.

Purchasing health insurance coverage (only if you are not already covered).

To claim one of these exceptions, you will need to complete IRS Form 5329 along with your income tax returns the following year. Even if you avoid the penalty, you will still need to pay taxes on the money you withdraw. This means that you should withdraw enough to cover your needs, plus a little extra for taxes.

Is there a Roth IRA withdrawal penalty?

Yes, penalty-free early withdrawals for Roth IRAs apply to only two circumstances: first–time home purchase or death or disability of a family member. However, the penalty for early withdrawal from a Roth IRA only applies to earnings, since you have already paid taxes on the principal. You will also need to submit Form 5329 along with your tax return.

How do I avoid an early withdrawal penalty on 401(k) retirement funds??

It is possible to make early withdrawals from a 401(k). However, the IRS is especially harsh on early withdrawals from 401 (k) funds. You may make what are known as hardship withdrawals before age 59 ½ for the following reasons:

Purchase a first home.

Pay for college for yourself or a dependent.

Prevent foreclosure or eviction from your home.

Cover unreimbursed medical expenses for yourself or a dependent.

However, hardship withdrawals from a 401 (k) differ from hardship withdrawals from an IRA. You will be assessed a 10 percent penalty in addition to paying income taxes on your withdrawal. To avoid the 10 percent penalty on early withdrawals from a 401(k), you must fulfill one of the following circumstances.

Total disability.

Medical expenses that total more than 7.5 percent of your adjusted gross income (AGI).

Court order to give the money to a divorced spouse, child, or other dependents.

Permanent separation from your job (including voluntary termination) during or after the year you turn 55.

Permanent separation at any age with a plan for equal yearly distributions of your 401(k) (once you begin taking distributions, you must continue them until you reach age 59 ½ or for five years, whichever is longer).

A better option than a hardship withdrawal from your 401(k) may be to take a loan against the value of your 401(k) with an outside lender. The lender places a lien against your 401(k) which remains in place until you repay the loan. Your funds remain in your 401(k), safe from the reach of Uncle Sam. However, if you default on the loan, the lender will have the right to seize your 401(k) to collect payment.

Is it bad to withdraw from an IRA?

It should be clear that IRA and 401k withdrawal should be considered a last resort. Even if you avoid tax penalties, you are depleting the available funds available for your retirement so in this sense, it is a bad idea and if you can avoid it, you should. If you must borrow, borrow enough to cover your obligations plus taxes, and repay the funds as quickly as possible. After all, you are actually repaying yourself – and your future.

Need to speak with a licensed tax professional? Optima Tax Relief provides a comprehensive range of tax relief services. Schedule a consultation with one of our professionals today.

Tax Evasion, Fraud & the Statute of Limitations on Tax Crimes

Tax evasion and fraud is not just a problem for white-collar crime criminals. Filing your taxes, particularly if you have considerable assets or run your own business, can be terribly complex. This means that the line between an aggressive – but legal – tax planning strategy and fraud is thinner than you might think.

Perfectly innocent mistakes may be interpreted by an IRS investigator as suspect. Therefore, even if you are a law-abiding taxpayer it pays to know the difference between tax evasion and tax fraud, the penalties, and what the IRS’ statute of limitations is when prosecuting tax crimes.

Tax Evasion vs. Tax Fraud

Although often used interchangeably, there are important differences between tax evasion and tax fraud. Tax evasion refers to the use of illegal means to avoid paying your taxes. This includes felonies, such as refusing to pay your taxes once they have been assessed, and misdemeanors; such as failing to file a return. Tax fraud, on the other hand, refers to lying on your tax return and falsifying tax documents- which is always a felony charge. This can extend to tax scammers will pose as a tax preparers and then rip off customers through refund fraud or identity theft. These phony accountants are committing Accountant Fraud and will tell you that they can get you a large tax refund and typically prey on low-income and non-English speaking taxpayers.

Take for example celebrity-convict Wesley Snipes, who was charged with three counts of failing to file a return. Snipes was convicted for three misdemeanor charges and received the maximum one-year sentence for each count. If he had been found guilty of a felony evasion charge or of tax fraud, he could have received up to five years for each count.

Statute of Limitations for Tax Evasion or Tax Fraud

The statute of limitations of a crime is the amount of time a prosecutor or a plaintiff has to file charges. In the case of taxes, it represents how long you should be looking over your shoulder after – willfully or otherwise – lying on your tax return.

The general rule of thumb is that the IRS has three years to audit your tax returns. If an investigation of your tax return reveals you concealed over 25% of your income, the IRS gets twice the time, six years, to file charges. However, this time period can be extended for a variety of reasons.

How can the Statute of Limitations be extended?

There are some stipulations that can make those ten years spread out to an even longer period of time. Here are some reasons you may have an extended tax statute of limitations:

If you agree to an extension, your statute is placed on hold until that extension time is up.

If you file bankruptcy, your statute is placed on hold until six months after the bankruptcy and court proceedings have been finished.

If you leave the country for at least six months, the statute is placed on hold until you decide to return.

If you are making payment installment arrangements or request innocent spouse relief, the statute is placed on hold until the final decisions are made.

For instance, if you are not in the United States or you become a fugitive, the statute of limitations may be “tolled” – or stop running – until you are found or return home. Another matter to consider is when the 6-year period starts. The IRS could prosecute a series of fraudulent tax returns as a single charge and only start counting the six-year period from your last act of tax evasion or fraud.

It gets worse. Although the IRS is limited to how far back it can look when filing charges in criminal court, there is no statute of limitations for civil tax fraud. This means the IRS can look back as far as it wants when suing for civil fraud. In practice the IRS rarely goes back more than six years because it has a high enough burden of proof to meet in fraud cases without having to deal with the added difficulties of proving older charges.

Tax Crime Statistics

Let’s end with the good news. Although the law grants extensive powers to the IRS, the chances of you being charged — never mind convicted — of tax fraud are minimal. According to IRS statistics, of the approximately 240.2 million tax returns filed, less than 2,000 people were investigated for fraud in 2020. Of those who were investigated, only half were actually charged with a criminal offense. However, once the IRS charges a taxpayer, the conviction rate is high: around 93%. Tax prosecutors have a high burden of proof to meet and their resources are limited; so they tend to focus their efforts on clear-cut cases.

Another positive tidbit is that the IRS rarely brings up an original return in audits or criminal prosecutions, if you came forward and tried to correct mistakes through an amended return. This means that if you avoid blatant abuses and correct filing errors when they come up in an audit, your chances of staying on the right side of a prison cell are excellent.

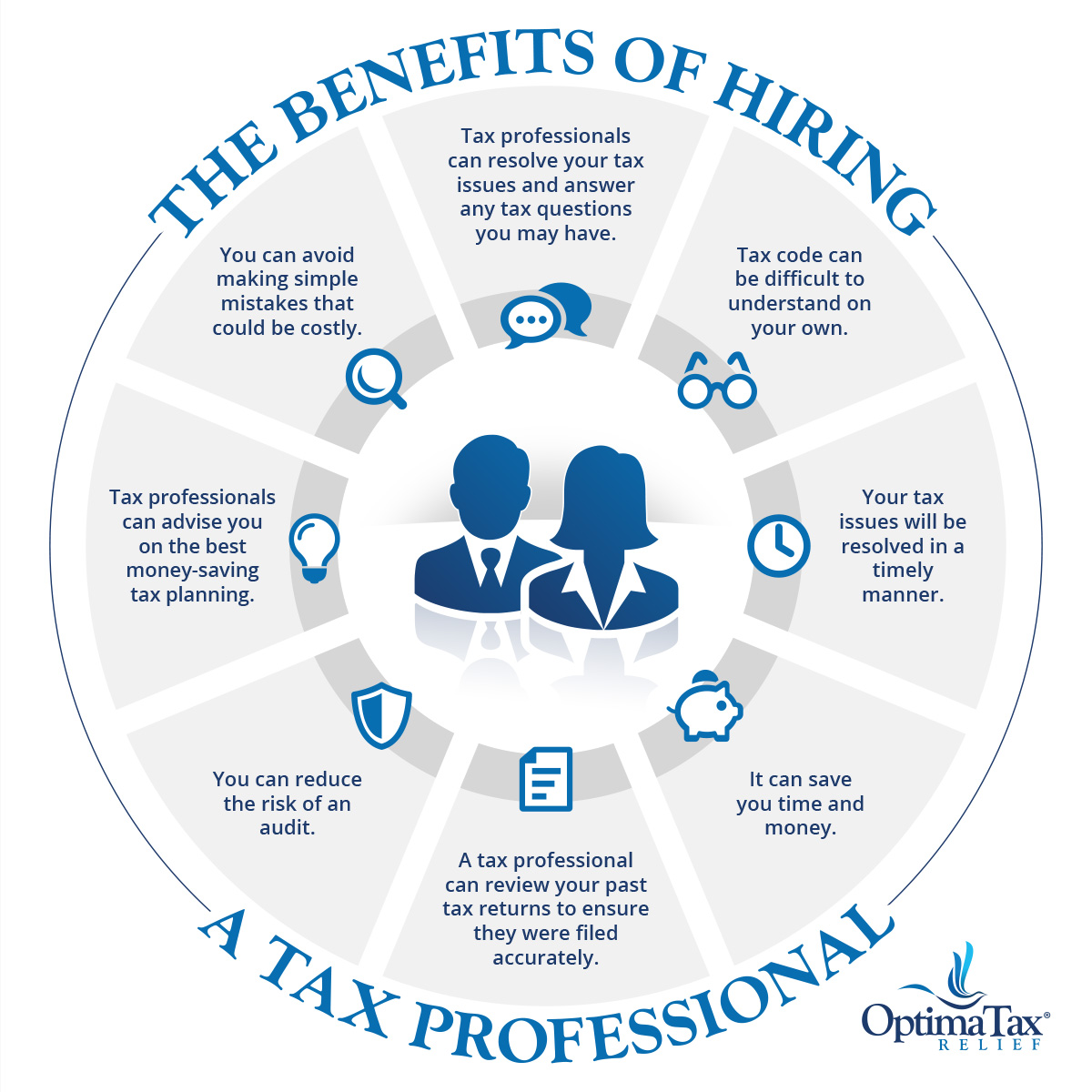

Most people require assistance when it comes to preparing and filing a tax return. Some may even find themselves having to provide additional information to the IRS and do not know what it is or where to find it.

Hiring a tax professional could save individuals both time and money when dealing with the IRS. Tax professionals can also prepare tax returns, help file income taxes, and assist taxpayers when it comes to dealing with the IRS, tax notices, tax liabilities, audits, and more.

Types of Tax Professionals

There are various types of tax professionals who specialize in focused areas of tax relief or tax prep and carry specific professional licenses.

Certified public accountants or CPAs can provide a variety of services such as:

Maintaining financial records.

Examining financial statements.

Providing auditing services.

Preparing tax returns.

Some CPAs specialize in tax planning and preparation such as:

Tax audits.

Payment and collection issues.

Appeals.

Enrolled agents are trained to find federal tax matters and are licensed by the IRS. Enrolled agents can assist with the following:

The preparation of both individual and business tax returns.

The representation of clients.

Other aspects of being a tax professional.

A tax attorney is licensed by the state to practice law. Most states require an attorney to have a law degree and pass a test administered by the state (bar exam). Tax attorneys can assist taxpayer with:

The preparation of tax returns.

Tax planning.

Providing advice to clients on long-range strategies for reducing their taxes.

Like CPAs and EAs, tax attorneys have unlimited rights to represent a client before the IRS.

Areas of expertise

There are a range of services that tax professionals can provide to taxpayers that can help them understand their taxes better. Based on what service you need, choosing the right tax professional or tax preparer can help you get back on track with your taxes, small business, and much more.

Enrolled Agents are IRS-authorized tax professionals who work alongside the U.S. Department of the Treasury by providing representation to individuals who need tax assistance.

Certified Public Accountants (CPAs) have state certifications to practice accounting. These experts can help individuals navigate certain tax situations. CPAs are licensed to represent taxpayers before the IRS.

Retirement tax professionals can help individuals know how their retirement options will impact their taxes. These types of tax professionals have received advanced training in tax preparations specifically for retirement plan contributions, distributions, and rollovers.

Small Business/Sole Proprietor tax professionals specialize in working with small businesses’ tax returns and educate their clients on how to properly prepare both their personal and company returns. These types of tax professionals have specialized training in sole proprietors, partnerships, and S corporations.

Investment Income tax professionals specialize in big or small investments, and gains or losses. These tax professionals also show your current and future tax situations.

International Taxation tax professionals assist individuals who have lived or worked abroad. These tax professionals are trained in international taxation which includes, claiming foreign earned income exclusions, the foreign tax credit, or treaty benefits for nonresident aliens.

Professional Licenses

Enrolled Agents (EAs) and Certified Public Accountants (CPAs) are both experienced professionals who maintain high ethical standards. The main difference between an EA and CPA is that an EA specializes specifically in taxation. CPAs can provide a wider scope of tax services for individuals.

Working with an EA would be beneficial for those who have IRS issues such as individuals who are in collections or dealing with an audit with the IRS. An EA would be best suited for someone who needs assistance with the IRS to help them with their tax concerns. EAs are also a great option for those who need tax preparation assistance and planning advice for both individuals and businesses.

CPAs specialize in tax preparation that can help individuals identify both their credits and deductions that can help them qualify for an increase in their refund or help lower their tax bill. CPAs are also beneficial if someone needs their tax information compiled, reviewed, or audited.

When should I hire a Tax Professional?

You should hire a tax professional if you are short on time, are unsure how to file your taxes correctly, or feel overwhelmed by IRS forms with preparing your taxes. Tax professionals can help answer tax questions that you may have and even resolve most tax issues you may have.

The tax code can be very complicated and if you are unsure on how to handle your tax matters, a tax professional can assist. For example, a tax professional can help reduce the risk of any audit and know how to deal with the IRS on your behalf if you do end up being audited. Tax professionals can also help taxpayers avoid making costly mistakes on their tax return such as missed deductions or triggering an IRS letter. Tax professionals can also review previous tax returns to see if there were any errors and needs to be amended.

How to find the right Tax Professional for you

Individuals searching for tax assistance should follow these steps in order to find a tax professional who best fits their needs:

Confirm your preparer has a tax identification number (ITIN).

Make sure to confirm tax fees to ensure you are not being overcharged.

Avoid tax preparers who do not e-file tax returns.

Make sure that your tax preparer signs their name and provides their Preparer Tax Identification Number (PTIN) on your tax return.

Make sure your tax professional can respond to the IRS. Enrolled agents, CPAs and attorneys that have a PTIN can represent you when it comes to IRS audits, payments, and collection issues.

10 Questions to ask a Tax Professional

Do you have an IRS-issued Preparer Tax Identification Number (PTIN)?

How do you keep up with the latest tax law? Are you regularly taking education courses?

Do you offer a free initial consultation?

Will you be the one preparing my return or someone in your office?

Do you offer IRS e-file, and will my tax return be submitted to the IRS electronically?

Will you keep my records and receipts on file? How long will you keep my records for?

When do you require payment?

When can I expect to receive my completed tax return?

What happens if I get audited?

Do you outsource your tax preparation?

Things to look out for when hiring a Tax Professional

Taxpayers should be aware of any red flags they experience when looking to hire a tax relief professional. Here is what individuals should look out for before hiring a tax professional:

Check the preparer’s qualifications.

Review the preparer’s history.

Ask about services and fees.

Make sure that the preparer offers e-filing.

Ensure your preparer has open availability if you have additional questions regarding your taxes.

Never sign a return if your preparer has added their name or PTIN.

How much does it cost to hire a Tax Professional?

The average cost of hiring a tax professional will depend on the complexity of the case that they are working on.

Consequences of not Hiring a Tax Professional

The federal tax penalties you could face by not hiring a tax professional to help you prepare your taxes could far outweigh the cost of soliciting tax help. Here are the repercussions individuals could face if they choose to not hire a tax professional:

Filing your own taxes could be time-consuming and confusing if you have never filed before.

You can miss out on tax preparation fees that could have been deductible.

You could miss out on certain credits or deductions if you are not aware of them.

If you get audited, you will not have a tax professional that can assist you through the process.

Filing your own taxes could lead to you making avoidable mistakes that could cause you problems with the IRS down the road.

Tax Relief Services at Optima Tax Relief

Optima Tax Relief offers tax relief services to individuals who are struggling with their IRS or state tax debt. Taxpayers that need assistance with tax preparation, setting up a payment plan with the IRS, getting out of collections, resolving an audit, or are looking to see if they qualify for a possible reduction in their total tax debt, should consider using Optima’s services.

The IRS and the Treasury Department have already begun to distribute a second round of stimulus checks to individuals. For those who opted for direct deposit, they can expect to receive their money very soon if they haven’t already. Taxpayers who are receiving their economic impact payment in check form, can expect to receive it throughout all of January.

If Student Loan Forgiveness is Adopted, it Could Impact Your Taxes.

Student debt cancellation is currently being discussed between Senate Minority Leader Chuck Schumer and President-elect Joe Biden. Because of the ongoing pandemic, many Americans are struggling to financially stay afloat because of the ongoing pandemic. Student loan relief could help those who don’t have the ability to make their monthly payments. Here are some possible tax implications you could face if your student debt goes away.

Although the stock market has been unstable throughout the course of the pandemic, millions of individuals have still been investing in stocks and making the most of stock prices that have hit their lowest. Those who have been investing in the stock market or have sold any stock will need to report any capital gains they received to the IRS in order to avoid any tax implications.

Small Businesses have been hit with a PPP tax Change. Here’s Everything You need to Know.

The IRS has added additional information to the Small Business Administration’s Paycheck Protection Program. The additional details entail that tax-deductible items will not be deductible if they were paid through PPP funds.