Tax Evasion, Fraud & the Statute of Limitations on Tax Crimes

Tax evasion and fraud is not just a problem for white-collar crime criminals. Filing your taxes, particularly if you have considerable assets or run your own business, can be terribly complex. This means that the line between an aggressive – but legal – tax planning strategy and fraud is thinner than you might think.

Perfectly innocent mistakes may be interpreted by an IRS investigator as suspect. Therefore, even if you are a law-abiding taxpayer it pays to know the difference between tax evasion and tax fraud, the penalties, and what the IRS’ statute of limitations is when prosecuting tax crimes.

Tax Evasion vs. Tax Fraud

Although often used interchangeably, there are important differences between tax evasion and tax fraud. Tax evasion refers to the use of illegal means to avoid paying your taxes. This includes felonies, such as refusing to pay your taxes once they have been assessed, and misdemeanors; such as failing to file a return. Tax fraud, on the other hand, refers to lying on your tax return and falsifying tax documents- which is always a felony charge. This can extend to tax scammers will pose as a tax preparers and then rip off customers through refund fraud or identity theft. These phony accountants are committing Accountant Fraud and will tell you that they can get you a large tax refund and typically prey on low-income and non-English speaking taxpayers.

Take for example celebrity-convict Wesley Snipes, who was charged with three counts of failing to file a return. Snipes was convicted for three misdemeanor charges and received the maximum one-year sentence for each count. If he had been found guilty of a felony evasion charge or of tax fraud, he could have received up to five years for each count.

Statute of Limitations for Tax Evasion or Tax Fraud

The statute of limitations of a crime is the amount of time a prosecutor or a plaintiff has to file charges. In the case of taxes, it represents how long you should be looking over your shoulder after – willfully or otherwise – lying on your tax return.

The general rule of thumb is that the IRS has three years to audit your tax returns. If an investigation of your tax return reveals you concealed over 25% of your income, the IRS gets twice the time, six years, to file charges. However, this time period can be extended for a variety of reasons.

How can the Statute of Limitations be extended?

There are some stipulations that can make those ten years spread out to an even longer period of time. Here are some reasons you may have an extended tax statute of limitations:

If you agree to an extension, your statute is placed on hold until that extension time is up.

If you file bankruptcy, your statute is placed on hold until six months after the bankruptcy and court proceedings have been finished.

If you leave the country for at least six months, the statute is placed on hold until you decide to return.

If you are making payment installment arrangements or request innocent spouse relief, the statute is placed on hold until the final decisions are made.

For instance, if you are not in the United States or you become a fugitive, the statute of limitations may be “tolled” – or stop running – until you are found or return home. Another matter to consider is when the 6-year period starts. The IRS could prosecute a series of fraudulent tax returns as a single charge and only start counting the six-year period from your last act of tax evasion or fraud.

It gets worse. Although the IRS is limited to how far back it can look when filing charges in criminal court, there is no statute of limitations for civil tax fraud. This means the IRS can look back as far as it wants when suing for civil fraud. In practice the IRS rarely goes back more than six years because it has a high enough burden of proof to meet in fraud cases without having to deal with the added difficulties of proving older charges.

Tax Crime Statistics

Let’s end with the good news. Although the law grants extensive powers to the IRS, the chances of you being charged — never mind convicted — of tax fraud are minimal. According to IRS statistics, of the approximately 240.2 million tax returns filed, less than 2,000 people were investigated for fraud in 2020. Of those who were investigated, only half were actually charged with a criminal offense. However, once the IRS charges a taxpayer, the conviction rate is high: around 93%. Tax prosecutors have a high burden of proof to meet and their resources are limited; so they tend to focus their efforts on clear-cut cases.

Another positive tidbit is that the IRS rarely brings up an original return in audits or criminal prosecutions, if you came forward and tried to correct mistakes through an amended return. This means that if you avoid blatant abuses and correct filing errors when they come up in an audit, your chances of staying on the right side of a prison cell are excellent.

Individuals that earned income throughout the tax year have the option to make non-deductible (after-tax) contributions to an IRA and benefit from tax-deferred growth. One of the most common risks that taxpayers take is paying additional taxes when withdrawing their money from their retirement accounts. Before making after-tax contributions to a traditional IRA, it is important for taxpayers to have an understanding of the rules and how to avoid the double tax trap on withdrawals.

There are certain contribution rules and limits that most taxpayers are not aware of with the IRA withdrawal process. Here are the rules taxpayers need to know about when making non-Roth after-tax IRA contributions:

Individuals are required to have earned an income.

The deductibility phase-out is determined on the filing status, income, and whether or not an individual is eligible to participate in a retirement plan at work.

Contribution limits are the lesser of: $6,000 (plus $1,000 if age 50+) or earned income and apply to aggregate additions to IRAs.

Certain financial institutions where an IRA is kept could cause certain issues such as the institution restricting an individual to add more than $6,000 per tax year. Banks also do not track, report, or verify if an individual made a pre-tax or non-deductible IRA contribution. The responsibility is left up to the taxpayer.

For those who choose to make after-tax contributions to an IRA, are required to give the IRS a heads up that they have already paid taxes on those dollars by using Form 8606. Individuals who fail to report, track, and file the form will most likely lose the ability to shield part of their IRA withdrawal from a tax penalty when the money is withdrawn.

Optima Tax Relief provides assistance to individuals struggling with unmanageable IRS tax burdens. To assess your tax situation and determine if you qualify for tax relief, contact us for a free consultation.

As the spirit of generosity is in the air, companies and employees need to know that holiday bonuses are considered supplemental wages and subject to taxes. Holiday bonuses are viewed by the IRS as compensation, just like paychecks, so taxes need to be withheld from your holiday bonus.

How Much are Holiday Bonuses Taxed?

Some of the taxes you will need to pay on your holiday bonus include:

Social security tax:

You pay social security tax on all compensation up to $132,900 in 2019. If you haven’t passed this threshold, then you can expect your employer to deduct 6.20% from your bonus for social security.

Medicare tax:

You can expect another 1.45% to be deducted from your holiday bonus for Medicare tax.

Federal income tax:

The IRS requires a set percentage of your bonus to be withheld when you receive it. This is because your holiday bonus is considered a supplemental income. Under tax reform, the federal tax rate for withholding on a bonus was lowered to 22%. This is lower than the federal income tax rate of 25%.

State income tax:

depending on which state you live in, state income tax will be withheld at the rate the state requires by law.

Retirement Plans (401k):

If you have requested that your employer contribute a portion of your wages to your retirement plan, then the rate at which you have set will be the same rate that will be taken out of your holiday bonus.

Ultimately, you should check with your employer about your holiday bonus and taxes. Your employer has the option to combine your regular paycheck and holiday bonus and withhold taxes on the whole amount. If your employer does this, it may result in a higher withholding than 22%.

If this is the case, don’t worry as you will eventually get some of the money back as part of your federal tax refund when you file your taxes.

How to Avoid Holiday Bonus Tax

Are there any ways to avoid paying tax on the bonus? No. And failing to report and pay taxes could lead to problems down the road. But there are ways to minimize or delay the impact. Here are three options:

Give a little more:

Employers can estimate the taxes an employee would have to pay on the bonus and add that to the total amount. That way, after taxes, the employee would get to keep the intended bonus amount. Obviously, this requires the employer to be more generous, which is not always possible.

Invest in the future:

Another option – that would avoid both payroll and income taxes – is to put the bonus into the employee’s 401K retirement plan. While employees would not actually receive a check during the holidays, they would also not have to pay taxes on that money until they withdraw it. In the meantime, that bonus could continue to grow.

Kick Off a Healthy New Year:

Employers can decide to award holiday bonuses in January and offer the option of placing the money in a Flexible Spending Account for healthcare. None of that money would be taxed, but the employee would have to use it on qualifying health or dependent care expenses.

If you’re an employee and your company will not offer any of the options above, then do your best to plan ahead and factor the taxes into your holiday budget. And if it makes you feel any better, giving is always better than receiving.

Looking for assistance with tax relief? Optima Tax Relief’s licensed professionals offer a range of tax services to help you. Reach out for a consultation today.

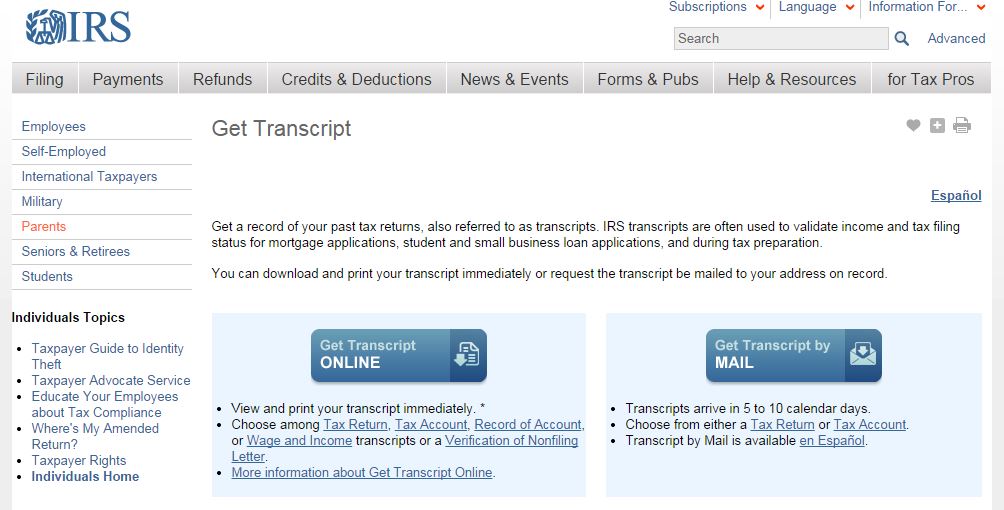

Getting a copy of your IRS transcript is easy and can be done entirely via the IRS.gov website. Follow these simple steps to retrieve your tax transcript.

Keep in mind that only transcripts for filed taxes are available. For example, if you did not file in 2003, there won’t be a tax transcript for that year. Also, if the IRS has not finished with your taxes, the transcript will not be available until they have completed those taxes.

What is an IRS Transcript used for?

IRS transcripts are typically used to validate past income and to prove income to lenders. They are often used to determine status for mortgage, student, and small business loan applications and help with tax preparation.

What information is on an IRS Transcript?

An IRS transcript includes most line items from your tax return, including all accompanying forms and schedules, as it was originally filed. Any changes made after the original filing will not be reflected. Key information listed on transcripts include marital status, AGI, taxable income, payment methods, and W-2 information.

How to get your IRS Transcript Online

You can request tax transcripts online for the current tax year and the three prior tax years. To request older transcripts, you’ll need to submit Form 4506-T. To request a transcript online:

Look under the Tools tab that is part way down the web page. Click: Get transcript for your tax records.

Once you reach the transcript page, you can request to get them by mail or continue getting them online by clicking on the box to the left, Get transcript online.

If you have gotten transcripts before, you can sign in. If not, you will need to click on the right side to create an account: Sign up.

Complete the sign up process and log in.

The next page will show a drop-down menu and ask why you need the transcript. Choose the answer that best fits your needs and continue. They ask you what you need it for so they can help you pick the right transcript.

The next page lists all your transcripts, in four different categories for all the years you filed. These include Tax Return Transcript, Record of Account Transcript, Account Transcript, and Wage and Income Transcript.

Select the transcript you need for the right year.

The site will automatically generate a PDF file of your transcript. Print it and save it.

Log out completely or close the browser when you are finished.

Make sure your pop-up blocker is off for the IRS site. It can cause errors when trying to retrieve your transcripts. If you chose mail, allow 5 to 10 business days for them to arrive before requesting another.

If you have problems navigating the website, you can contact the IRS for further assistance at 1-800-829-1040. For further assistance or help with a different tax issue, contact Optima Tax Relief. Optima Tax Relief offers a comprehensive range of tax relief services. Schedule a consultation with one of our professionals today.

Optima Tax Relief provides assistance to individuals struggling with unmanageable IRS tax burdens. To assess your tax situation and determine if you qualify for tax relief, contact us for a free consultation.

If you’re debating whether or not to donate to charity, it’s important to understand the tax benefits and tax-saving opportunities that could be available to you. Here’s a breakdown of what you need to know when understanding what you could qualify for when it comes to charitable donations.

Some donations may not be eligible for deductions. In order to make a donation, it must be to a charity with a tax-exempt status determined by the IRS. This means that charitable donations cannot be made to friends, relatives, or groups that do not fall under the tax exempt status. The list of approved organizations are the following:

A community chest, corporation, trust, fund, or foundation, organized or created in the United States or its possessions, or under the laws of the United States, any state, the District of Columbia or any possession of the United States, and organized and operated exclusively for charitable, religious, educational, scientific, or literary purposes, or for the prevention of cruelty to children or animals.

A church, synagogue, or other religious organization.

A war veterans’ organization or its post, auxiliary, trust, or foundation organized in the United States or its possessions.

A nonprofit volunteer fire company.

A civil defense organization created under federal, state, or local law (this includes unreimbursed expenses of civil defense volunteers that are directly connected with and solely attributable to their volunteer services).

A domestic fraternal society, operating under the lodge system, but only if the contribution is to be used exclusively for charitable purposes.

A nonprofit cemetery company if the funds are irrevocably dedicated to the perpetual care of the cemetery as a whole and not a particular lot or mausoleum crypt.

Some contributions may lead to only a partial credit. For particular donations, a taxpayer will only receive a portion of a credit. For example, if you purchase a shirt that is a part of a charitable cause, the entire price of the shirt is not deductible. The fair market value must be determined and subtracted from the cost of your purchase in order to determine the amount of your donation.

When determining how much of a charitable donation you would like to make, it is important to know there is a limit on all donations you make throughout the tax year. Total charitable contributions are generally limited to no more than 50% of your adjusted gross income.

If you need tax help, contact us for a free consultation.

The United States federal income tax system is operated under a system of voluntary compliance. This innocuous sounding term actually packs quite a potent punch – there is little that is voluntary about the federal tax system, at least where paying taxes is concerned. Many celebrities and ordinary citizens alike have learned this lesson the hard way, almost always at great financial cost.

Voluntary Compliance and Audits

The “voluntary” nature of taxation relates to the method of submitting and paying income tax obligations. The Treasury department places the burden of figuring, reporting and paying income taxes in the hands of its citizens, rather than automatically collecting the revenue. In contrast, sales taxes and other use taxes are involuntary. Whenever you buy an item or service that carries sales tax, you not only pay the price of the merchandise or service, but the tax as well.

Although the IRS collects taxes under a voluntary compliance system, the assumption is that most of the population will fail to pay its full tax burden, either by mistake or by deliberate attempts at tax evasion. To remedy the resulting shortfall, the IRS has instituted a system of tax audits. A majority of audits are triggered by suspicious items included or omitted from tax returns. Other tax audits are generated because taxpayers who should file tax returns fail to do so or file so-called frivolous returns. An unfortunate minority of taxpayers are flagged for audits by random selection – just plain bad luck.

Celebrity Tax Evasion & Frivolous Tax Returns

Throughout history, famous and infamous figures have been caught in the net of failure to comply with the “voluntary” system. Notorious gangster Al Capone died in prison as a result of a conviction of income tax evasion. More recently, celebrities like Martha Stewart, Wesley Snipes and Marc Anthony have been snared by convictions for federal income tax evasion. One persistent but thoroughly discredited strain of tax protest arguments claim that federal income taxes are unconstitutional, or that taxpayers can eliminate their federal income obligations by filing “zero” tax returns. Snipes was one of the more famous figures taken in by this line of reasoning, and as a result was convicted of misdemeanor tax evasion in 2008 and sentenced to 3 years in prison. As of 2014, the movie star was back on the silver screen, headlining in the action feature Expendables 3. Presumably, Snipes will pay a rightful proportion of his earnings from the film, marketed as a summer blockbuster, to the IRS. The IRS exercises little patience with taxpayers filing what it concludes to be frivolous returns. It imposes an array of civil penalties, listed below:

Accuracy-related penalty under section 6662 (20 percent of the underpayment attributable to negligence or disregard of rules or regulations)

Civil fraud penalty under section 6663 (seventy-five percent of the underpayment attributable to fraud)

Erroneous claim for refund penalty under section 6676 (twenty percent of the excessive amount)

Fraudulent failure to timely file income tax return (triple the amount of the standard failure to file addition to tax under section 6651(a)(1))

Frivolous submissions other than tax returns under the Tax Relief Health Care Law of 2006 ($5,000 penalty)

Is Tax Evasion a Felony?

Criminal penalties for tax evasion based on frivolous tax returns can be severe. Both fines and jail time may be imposed upon conviction. Specific penalties are listed below.

Felony for attempting to evade or defeat tax under Section 7201 provides as a penalty a fine of up to $100,000 ($500,000 in the case of a corporation) and imprisonment for up to 5 years with optional additional fine up to $250,000

Felony for willfully making and signing under penalties of perjury any return, statement, or other document that the person does not believe to be true and correct as to every material matter under section 7206 is a fine of up to $100,000 ($500,000 in the case of a corporation) and imprisonment for up to 3 years with optional additional fine up to $250,000

Felony for promoting frivolous arguments and assisting taxpayers in claiming tax benefits based on frivolous arguments under section 7206(2) may be fined up to $100,000 ($500,000 in the case of a corporation) and imprisonment for up to 3 years with optional additional fine up to $250,000

How Do Corporations Avoid Paying Taxes?

Individual taxpayers are far from alone in their attempts to minimize their tax burdens. Complex accounting maneuvers with names like the Double Irish or Dutch Sandwich allow major corporations like Apple and Google to evade the 35 percent US corporate tax. But unlike tax evasion or frivolous tax returns, corporate tax dodges are largely perfectly legal – for now. Governments around the world have begun to put measures in place designed to curb offshore tax havens and other corporate tax evasion strategies.

Fair Tax System

The voluntary compliance system is far from the only viable system of income taxation. The so-called fair tax system is based on imposing use taxes – the more goods and services a person uses, the more taxes he or she pays. But fair use systems often impose a heavier burden on low-income taxpayers because they pay a higher proportion of their income use taxes. For this reason, fair use taxes are often labeled as regressive — and aggressively unfair.

Simple Tax System

Supporters of a so-called simple tax system include tax expert Austan Goolsbee and policy wonk Ezra Klein. Under a simple tax system the IRS would calculate taxes, credits and deductions and provide taxpayers with a copy of the completed return. Taxpayers who agree with the IRS’s calculations could simply accept the return, while taxpayers who disagree could file their own returns.

The simple tax system has obvious advantages. The IRS has a good idea of what many taxpayers earn and owe anyway, thanks to Form W-2 and various versions of Form 1099. The simple tax system would also ensure nearly 100 percent compliance, since the IRS would be supplying tax returns rather than individual citizens.

As one might expect, the tax preparation industry (including TurboTax) largely disfavors the simple tax return system. Approximately 60 percent of all Americans contract with outside tax preparers to file their federal and state income tax returns. Implementing something like the simple tax system would cut deeply into that percentage.

While the simple tax return system is indeed simple, there are potential pitfalls. First, many taxpayers may accept the IRS’s version of their returns whether it is accurate or not from inertia, laziness or fear of reprisal. Second, even if the IRS and its agents were totally diligent in calculating the maximum credits and deductions, human error must still be considered.

Death and Taxes

Given the present financial and political climate, it is unlikely that the voluntary compliance tax system will change in the foreseeable future. It’s also a safe bet that attempts to evade taxes will continue, including extreme cases such as Facebook co-founder Eduardo Savarin, who renounced his American citizenship in 2012 shortly before the social media giant launched its IPO. In the face of such tax evasion attempts, the IRS will also undoubtedly continue its enforcement strategies, including the dreaded audit.

Considering a tax consultation? Optima Tax Relief offers a range of services discussed in our free consultation. Our award winning staff of tax professionals provide comprehensive tax relief services to help you resolve any tax issue. Speak to us today.